Sep 8th, 2022, 23:13

Sep 8th, 2022, 23:13

|

只看该作者 #5541 |

|

转啊 转啊转

注册日期: Jul 2007

帖子: 34,089

积分:5

精华:2

|

二级市场 和初级市场 不是一个东西吧,我们看到的soxl实时股价 是二级市场撮合价 它相对基金价值有交易溢价,但基金本身有些tricks维持自身股价绩效 SOXL是在纽交所arca交易的,纽交所不会给它做联动操作的啊 它得自己动 https://www.investopedia.com/terms/n/nyse-arca.asp NYSE Arca is an electronic stock and exchange-traded product (ETP) order matching platform |

|

|

|

Sep 8th, 2022, 23:35

|

只看该作者 #5548 | |

|

转啊 转啊转

注册日期: Jul 2007

帖子: 34,089

积分:5

精华:2

声望: 24936019

|

引用:

而且soxl 日中 也有好多时段 是没做到3x效果的, 就是关键点位 尤其收市价 有回归到 要是咱也会这种trick 那该多好啊 |

|

|

|

|

|

Sep 8th, 2022, 23:43

|

只看该作者 #5550 | |

|

Senior Member

注册日期: Jun 2006

帖子: 4,513

声望: 1177764

|

引用:

比较大众的SPY/SPXL,QQQ/TQQQ,SOXL等大盘ETF做的都在设计值。看到过一些加拿大公司的大盘ETF线性系数很差,不知道是流通性太差造成的,还是程序问题。 |

|

|

|

|

|

Sep 9th, 2022, 00:24

|

只看该作者 #5552 | |

|

Senior Member

注册日期: Jun 2006

帖子: 4,513

声望: 1177764

|

引用:

“Like its peer products, UVXY does not deliver leveraged returns on the VIX index itself, but on front- and second-month futures contracts.” 不知道如何查下月VIX指数,以及是否与它的设计指标相符。 感觉你是对比UVXY与当月VIX指数,发现它当日不是1:1.5关系。是个误解。 |

|

|

|

|

|

Sep 9th, 2022, 00:47

|

只看该作者 #5553 |

|

Senior Member

注册日期: Jun 2006

帖子: 4,513

声望: 1177764

|

这个链接里没有UVXY具体每日跟踪的VIX指数数据,但是给出了每天UVXY收盘价格与设计VIX涨跌幅1.5倍的系数差别数据:基本是一致的,在+-百分零点几波动(Premium/Discount)。 https://www.etf.com/UVXY#tradability |

|

|

|

|

Sep 9th, 2022, 01:44

|

只看该作者 #5554 | |

|

转啊 转啊转

注册日期: Jul 2007

帖子: 34,089

积分:5

精华:2

声望: 24936019

|

引用:

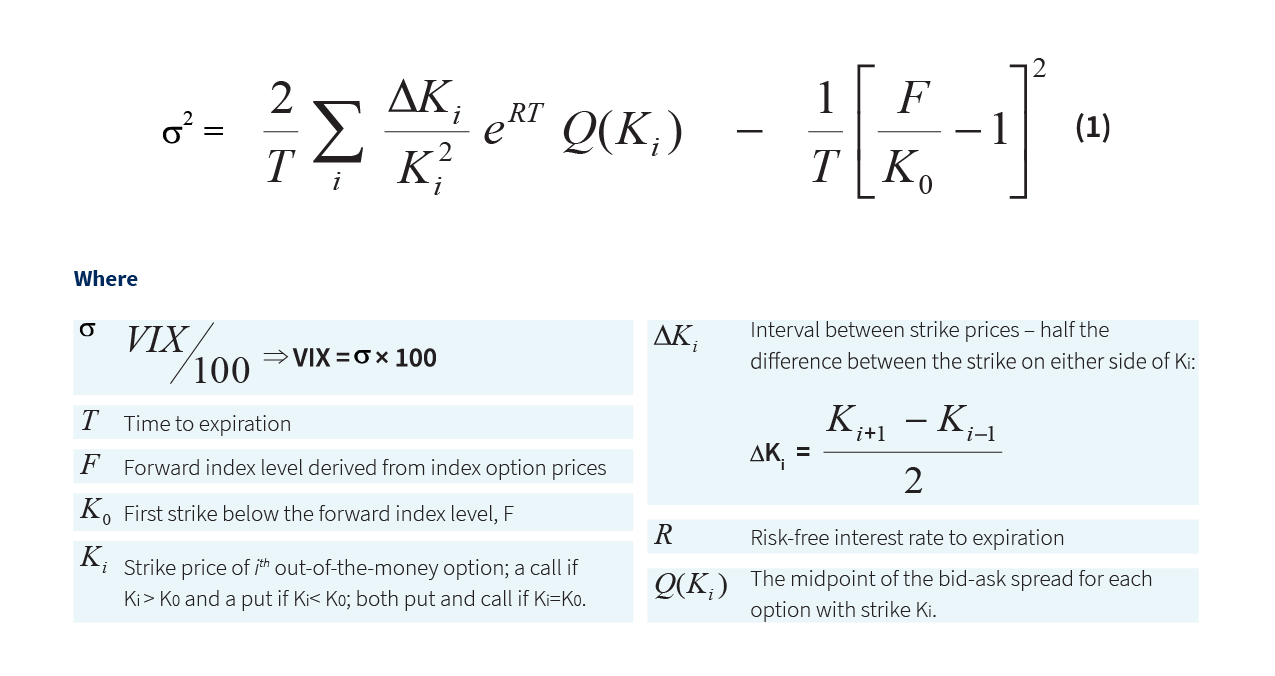

https://www.cboe.com/tradable_products/vix/faqs/ How is the VIX Index calculated? Cboe Options Exchange® (Cboe Options®) calculates the VIX Index using standard SPX options and weekly SPX options that are listed for trading on Cboe Options. Standard SPX options expire on the third Friday of each month and weekly SPX options expire on all other Fridays. Only SPX options with Friday expirations are used to calculate the VIX Index.* Only SPX options with more than 23 days and less than 37 days to the Friday SPX expiration are used to calculate the VIX Index. These SPX options are then weighted to yield a constant maturity 30-day measure of the expected volatility of the S&P 500 Index. * Cboe Options lists SPX options that expire on days other than Fridays. Non-Friday SPX expirations are not used to calculate the VIX Index. Intraday VIX Index values are based on snapshots of SPX option bid/ask quotes every 15 seconds and are intended to provide an indication of the fair market price of expected volatility at particular points in time. As such, these VIX Index values are often referred to as "indicative" or "spot" values. Cboe Options currently calculates VIX Index spot values between 3:15 a.m. ET and 9:15 a.m. ET (Cboe GTH session), and between 9:30 a.m. ET and 4:15 p.m. ET (Cboe RTH session) according to the VIX Index formula that is set forth in the White Paper. The generalized formula used in the VIX Index calculation is:

|

|

|

|

|

|

Sep 9th, 2022, 02:14

|

只看该作者 #5555 |

|

Senior Member

注册日期: Jun 2006

帖子: 4,513

声望: 1177764

|

期货合约有当月合约以及下月及再下月等不同期货合约,UVXY不是直接跟踪的主力当月合约形成的指数,而是跟踪的下月合约(更远一些的): “UVXY does not deliver leveraged returns on the VIX index itself, but on front- and second-month futures contracts.” 所以VIX index有多个。每天交易的合约有多个,常引用的VIX index是主力合约,不是中远期的((UVXY跟踪的)。 UVXY是给机构或保险机构用来对冲中远期价格风险的。 |

|

|

|

|

Sep 9th, 2022, 11:51

|

只看该作者 #5559 | |

|

转啊 转啊转

注册日期: Jul 2007

帖子: 34,089

积分:5

精华:2

声望: 24936019

|

引用:

但是最近 道指纳指和罗素波动太不同步,短炒uvxy难度很大,我扑了一次后 都不敢跟了,回归来慢薅Intel btu x 这些个股,稳当些 九月都不准备急进,十月风行稳定后再定下个计划。 新买那个房房 咱airbnb了,生意不错,有个找不到房子的$1800包了一间ensuite一个月,小亏 但有个人看家也好 |

|

|

|

|

|

|

|

请尊重文章原创者,转帖请注明来源及原作者。

凡是本站用户自行发布的任何信息,皆不代表本站的立场,

华枫网站不确保各类信息的正确性和可靠性,也不承担由此而导致的任何直接或间接损失以及任何法律责任。 |